By: Nick Hillman

For over three years—between March 2020 and September 2023—monthly payments on certain federal student loans were paused. The pause ended nearly a year ago, and many researchers and policy organizations want to know how the return to repayment is going for borrowers.

However, getting access to high-quality data on student loans is difficult. With the right data, we can learn how borrowers navigate repayment options, whether they are falling behind on payments, and what impact loans have on their daily lives. There is no comprehensive data source to capture all this information, so researchers must piece this puzzle together from multiple—and often limited—sources.

This post introduces a new data tool that helps fill in some of that puzzle. The tool is based on daily deposits from the U.S. Department of Education to the U.S. Treasury. These deposits are primarily made of student loan payments, allowing us to see trends in the pause and return to repayment.

Policymakers interested in understanding how the return to repayment is going for borrowers will find this tool useful. While it does not provide rich detail about repayment plans or borrowers’ characteristics, it does provide “real time” information to monitor and compare how the return to repayment compares to pre-pause trends.

What data exists to track the return to loan repayment?

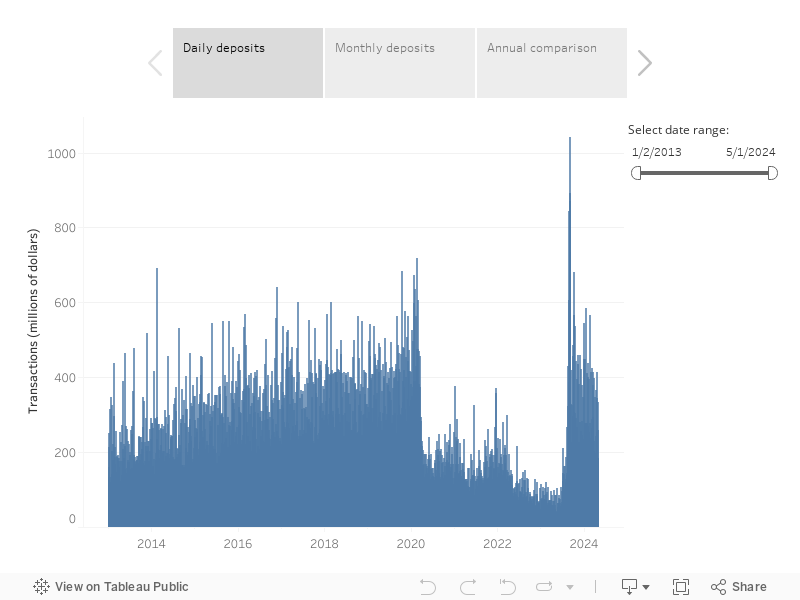

When borrowers make payments on certain federal student loans, these payments go to the U.S. Department of Education and in turn are deposited into the Treasury General Fund.

The Daily Treasury Statement (DTS) provides a public record of these transactions.

But extracting data from the DTS can be cumbersome, so the SSTAR Lab created an interactive tool that summarizes and visualizes these transaction records: the Student Loan Repayment Tool.

The Student Loan Repayment Tool allows users to see daily, monthly, or annual DTS deposits. It provides researchers with insights about how the return to repayment compares to pre-pause trends.

For example, this tool shows monthly deposits have been steadily trending downward since repayments resumed in the fall of 2023. After the initial spike when payments first came due, monthly deposits have steadily fallen.

How can this information help us learn about loan repayment?

We cannot decisively say “why” this downward trend is occurring—there are many potential explanations ranging from fewer borrowers in repayment or more participating in income-driven repayment plans, in forbearance, or in delinquency/default. The tool’s purpose isn’t to say “why” the decline is occurring. Instead, it shows that a decline is occurring. Without this information, researchers and policy analysts would not have a baseline to form their research questions, so the tool provides this baseline and can help spark research ideas and policy discussions around how the return to repayment is going for borrowers.

The U.S. Government Accountability Office (GAO) recently used a different source of data—student loan data from the U.S. Department of Education—to explore the return to repayment. They found approximately 18 million borrowers were currently in repayment in January 2024 and—among these borrowers—nearly half are either delinquent or in deferment or forbearance. Another third of these borrowers are in income-driven repayment plans with $0 payments. Researchers typically do not have access to the kind of data the GAO used in their report, so triangulating the DTS tool with findings using other data sources can help put the repayment puzzle together.

For more information about this tool and DTS data in general, we encourage readers to see the U.S. Department of Education’s comparison of DTS data to more granular data from the National Student Loan Data System (NSLDS). ED’s analysis shows Treasury’s DTS deposit data typically results in higher loan volume estimates but these estimates mirror NSLDS data very closely. Additionally, readers may consider analyses from the Federal Reserve Bank of New York and the Federal Reserve Bank of Philadelphia using DTS data helpful examples to see how these trends can be useful in policy deliberations.

Our research team found the DTS data to be an interesting and missing piece of the repayment puzzle, so we hope the Student Loan Repayment Tool can help spark research and policy ideas that lead to thoughtful and evidence-based discussions about student loan debt. It is just one piece of information that, when combined with others, can help us see how the return to repayment is going for millions of student loan borrowers.